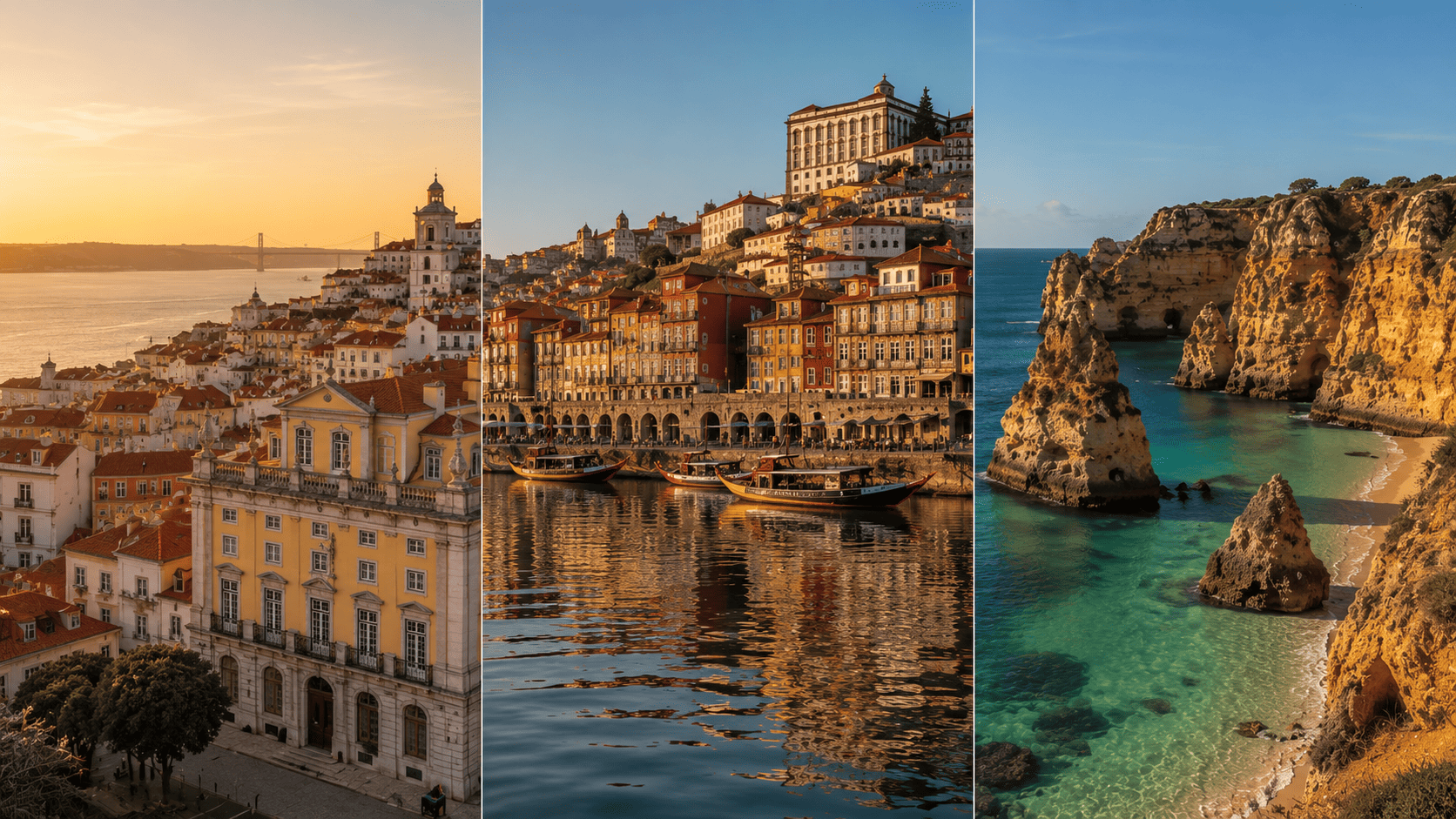

Portugal’s property market doesn’t move as one. National headlines—like the 17.5% year-on-year price jump recorded by Statistics Portugal (INE) in Q4 2025—can be misleading. Prices in inland Santarém have been climbing fast. But so have prices in Cascais and Foz do Douro, for completely different reasons, with different buyer pools and different risk profiles.

If you’re trying to decide where to put capital in 2026, the honest answer is: it depends on what you’re optimising for. Yield? Appreciation? Liquidity? A second home that also happens to generate income? Each of Portugal’s three main markets gives you a different trade-off.

Lisbon: Expensive, Tight, and Still Growing

Lisbon is the priciest market in the country. The municipality hit a median of €5,198/m² in Q4 2025, according to INE—and that’s across the whole city. Parishes like Santo António (home to Avenida da Liberdade) were trading at €6,819/m², up 16% year-on-year. New builds in the capital averaged €5,890/m², against €4,725/m² for existing stock.

Yet demand hasn’t cooled. Foreign buyers in Greater Lisbon paid 49% more per square metre than domestic buyers in Q4 2025 (INE). Knight Frank’s spring 2026 market note put prime residential values up 2.7% in 2025—slower than the pre-pandemic pace, but still positive—and forecast a further 4.5% rise through 2026. Savills anticipated luxury values rising 4–6% over the same period.

There are structural reasons prices keep moving. New housing supply in the capital is thin: roughly 2,000 units were delivered across Greater Lisbon in 2025 (Knight Frank). Planning restrictions in the historic centre mean developers can’t build their way out of the shortage. And the buyer pool keeps expanding—Americans, Brazilians, French, British, and GCC-based buyers are all active, drawn by residency routes (Portugal’s D2 and D7 visas remained open), lifestyle, and the city’s consistent positioning as a safe-haven market within Europe.

On yields: Gross rental yields in Lisbon range from roughly 2% to 6.4% depending on location and apartment size, with 1- and 2-bedroom units generating around 4.3% as of May 2026 (BestYieldFinder). Short-term rental regulation has tightened since December 2025—new Alojamento Local licences are restricted in high-density tourist zones—which caps upside for investors targeting Airbnb-style returns. Long-term rental demand is solid but rents have stopped accelerating: the average stood at €1,800/month in May 2026, unchanged year-on-year.

The entry point reflects all of that. At €599,900 median for an apartment and price-to-rent multiples of around 28 years, Lisbon has become a capital appreciation play as much as an income play—and buyers today are pricing in continued appreciation rather than yield alone. Investors who bought four or five years ago are sitting on strong unrealised gains, and the market’s track record of attracting international capital suggests that dynamic is unlikely to change quickly.

Porto: Better Value, Strong Fundamentals, One Major Catalyst Ahead

Porto’s pitch is straightforward: more city for less money, with a demand story that’s genuinely solid.

The average asking price in Porto sat at around €3,885/m² as of December 2025 (based on Idealista data), against Lisbon’s €5,900+. A 60m² apartment runs roughly €233,000; a 90m² family flat around €350,000. Gross rental yields in Porto city averaged 5.4% in Q4 2025, rising to 5.8% across the wider metropolitan area.

The demand base is diversified in a way that provides some cushion: Porto has over 80,000 higher education students, a growing tech and creative sector, consistent tourist arrivals, and rising interest from digital nomads and younger international buyers who find Lisbon financially out of reach. Vacancy rates in central neighbourhoods ran at 2–3% in early 2026.

The structural story is also interesting. Porto’s Ruby Metro Line (Vila Nova de Gaia) is already boosting values along its corridor. More importantly, the high-speed rail connection to Lisbon—first phase awarded October 2024—will cut the journey to around 75 minutes when complete. Infrastructure like that tends to reprice markets before it opens. That window is arguably still open.

The thing to understand about Porto is that the average masks a lot. Prices rose around 4.8% year-on-year from December 2024 to December 2025 city-wide, but the spread across neighbourhoods ran from -9% to +14%. Location selectivity matters more here than in Lisbon, where almost any central address has performed. Rent growth has also moderated—from double-digit increases in 2023–2024 to around 3% year-on-year in late 2025—which means the yield story is strongest in well-positioned assets rather than across the board.

Forecasts point to roughly 5% price growth across Porto municipality in 2026, with prime areas expected to outperform.

The Algarve: Lifestyle Premium, Tourism-Driven Yield, a Bifurcated Market

The Algarve is not one market. Quinta do Lago and Loulé are operating in a different universe from Tavira or the inland eastern municipalities. Understanding that split matters more than almost anything else if you’re allocating capital here.

At the prime end—the Golden Triangle (Quinta do Lago, Vale do Lobo, Vilamoura)—luxury villas outside developments averaged around €6,250/m² in mid-2025, with some properties crossing €10,000/m². Foreign buyers accounted for more than 80% of transactions in these locations. Americans specifically represented 37% of international luxury inquiries in 2025, up from 23% in prior years.

Across the broader region, the average asking price reached €4,385/m² in early 2026. Municipalities like Lagos (€5,066/m²) and Loulé (€5,672/m²) sit at the expensive end; inland areas like Alcoutim can still be found at €1,000–1,500/m².

Rental yields average 5.6% region-wide, with luxury short-term rentals in the Golden Triangle reaching 8% in peak segments. That’s the upside. The downside is regulatory creep—AL licensing restrictions are tightening, and in areas where short-term supply has outpaced demand, some yields are compressing.

Price appreciation ran at 9.3% year-on-year to August 2025, with Loulé, Lagos, São Brás de Alportel and Silves posting double-digit growth. Eastern Algarve “catch-up” markets like Tavira and Olhão have seen 25–40% appreciation over the last two to three years as buyers priced out of the west shifted east.

What makes the Algarve distinctive as an investment is precisely that dependence on international lifestyle demand—and how durable that demand has proven. Portugal’s tourism sector grew around 9% in 2025 and accommodation revenue in the region rose 6.5% over 2024. The Algarve isn’t chasing that audience; it’s already the destination. For investors, that means the income case is tied to a trend—experiential travel, climate migration, remote work relocation—that shows no sign of reversing.

A Quick Comparison

| | Lisbon | Porto | Algarve |

|---|

| Median price/m² (2025/26) | €5,198 | ~€3,885 | ~€4,385 |

| YoY price growth | ~8–10% | ~4.8% | ~9.3% |

| Gross rental yield | 2–6.4% | 5.4–5.8% | 5–8% |

| Primary buyer profile | International + domestic | Domestic + young international | International (lifestyle/tourism) |

| Key consideration | Premium entry point, income play | Location selectivity matters most | Lifestyle + income mix, know your zone |

| 2026 forecast | +4.5–5.5% | ~5% | +2–7% depending on location |

Sources: INE (Q4 2025), Idealista

So Which One?

There isn’t a universal answer, which is probably obvious by now.

Lisbon makes sense if you’re prioritising capital preservation and liquidity, and you’re comfortable with a lower current yield. It’s the most mature, most internationally liquid market in the country. You can exit. That matters.

Porto makes sense if yield is a priority and you believe the infrastructure thesis—that the high-speed rail and continued tech sector growth will push the market towards Lisbon pricing over the medium term. The entry point is still materially lower, and the income fundamentals are better right now.

The Algarve makes sense if your use case is mixed—part lifestyle asset, part income vehicle—and you have a view on tourism remaining durable. The Golden Triangle at the prime end is genuinely scarce. At the eastern Algarve end, there’s still relative value.

What doesn’t make sense is buying any of them without understanding what part of the market you’re actually buying into. Portugal’s headline numbers are strong, but the variance within each region is wide enough that the location decision—and increasingly, the neighbourhood and even the street—will determine whether the investment actually works.

– At Luznur Capital, we work with private buyers, investors, and corporate clients looking to acquire property or projects in Portugal — including Golden Visa and residency pathways. If you’d like a more tailored view of your options contact us: info@luznurcapital.com.